The operational reliance of the national insurance industry on the banking sector has entered an era of massive consolidation. According to data released by the Financial Services Authority (OJK) for March 2026, joint banking channels—commonly known as bancassurance—now firmly dominate the landscape, capturing 40.4% of total life insurance premium revenues in Indonesia. The OJK Executive Director of Insurance Supervision noted that this concentration reflects the deep integration between domestic banks and insurers utilizing widespread financial databases.

While automated payroll attachments and simple mobile banking integrations make purchasing insurance products incredibly easy for consumers, this ecosystem presents critical underlying risks for institutional clients. The OJK has issued direct warnings regarding field miss-selling. This occurs when frontline sales representatives pitch standardized insurance packages without fully analyzing the complex, specialized risk profiles of individual corporate entities.

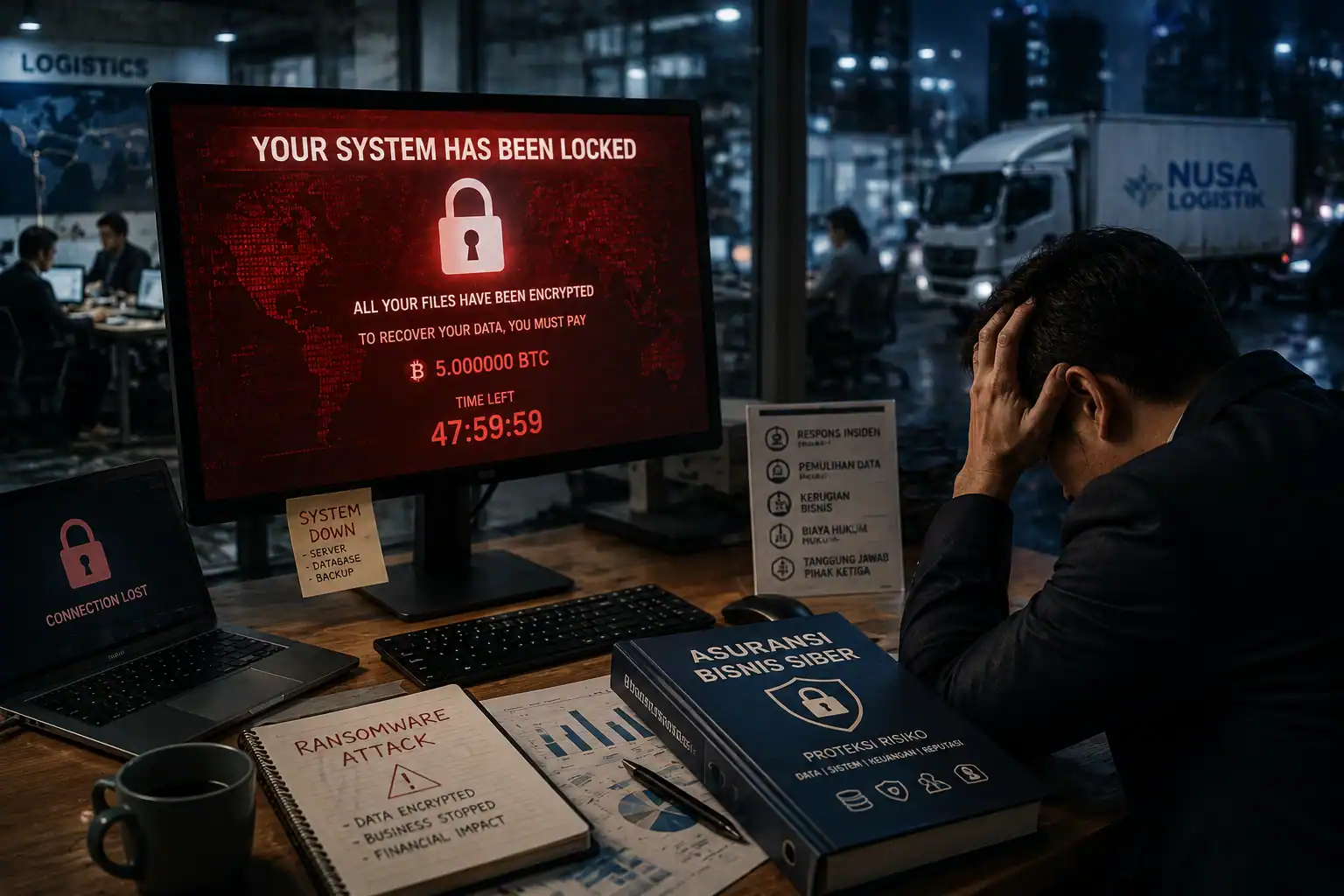

For entrepreneurs and directors, selecting commercial property insurance, liability coverages, or group employee benefits should never be treated like buying an off-the-shelf consumer item. Every enterprise faces a highly distinct combination of operational hazards. This environment requires the critical intervention of an objective corporate risk consultant operating with unwavering precision.

The Corporate Insurance Purchase Dilemma via Mass Channels:

- Advantages: Fast registration, directly tied to commercial bank accounts.

- Risks: One-size-fits-all coverage, high probability of claims being denied due to lack of deep technical risk profiling.

Securing an enterprise requires an exhaustive, precise audit of potential liabilities rather than treating safety as a superficial checkbox on an administrative form.

Frequently Asked Questions (FAQ):

- What exactly is the miss-selling risk highlighted by the OJK? It refers to instances where clients buy policies without a comprehensive understanding of core exclusions, deductibles, or specific payment terms.

- Why does my enterprise require a custom protection layout instead of standard packages? Because the physical liabilities of a food production facility differ fundamentally from a creative house or a technology network developer.

- How can we guarantee our corporate claims will be paid out seamlessly? By engaging specialized risk intermediaries to run technical policy cross-checks before commercial signatures are applied.

In conclusion, while banking network convenience is a fantastic modern asset, executing detailed due diligence on your commercial risk coverage remains an absolute operational imperative.

Sources:

- OJK / Stabilitas id — OJK March 2026 Data: Bancassurance Channels Control 40.4 Percent of Life Insurance Premiums — Stabilitas URL — Accessed May 30, 2026

Published: May 30, 2026

Source and editorial notes are managed through GATICORP CMS.